You've Been Using Agent-Like Capabilities for Decades

The Patterns that Predict If and How Agentic Commerce Will Scale

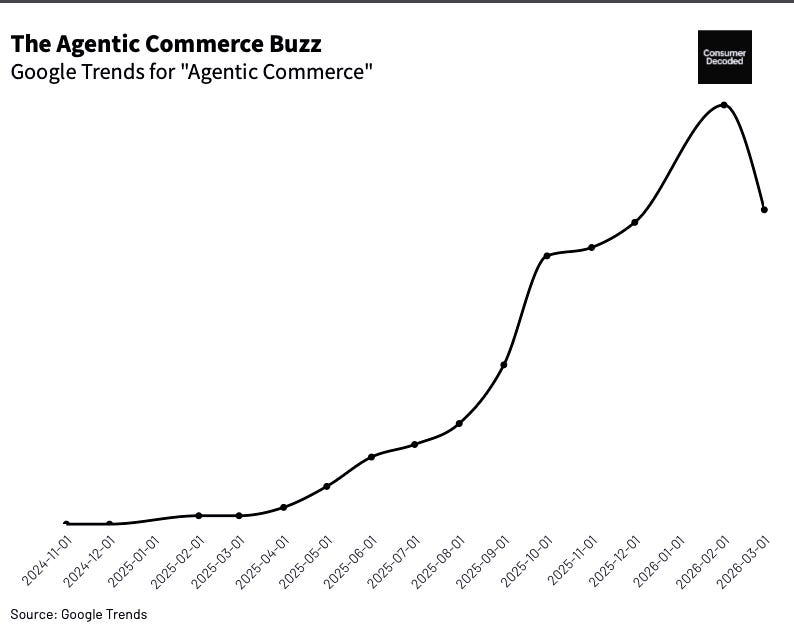

Two years ago, “agentic commerce” barely existed as a concept. Today, it’s everywhere—alongside a broader wave of AI speculation about how consumers will shop in the future.

There are clear patterns in history where consumers have simplified and then fully delegated their decision-making—often for decisions with much higher stakes than which toilet paper is being delivered.

These past cases may be the best insight into how agentic commerce will scale.

The Original Delegation

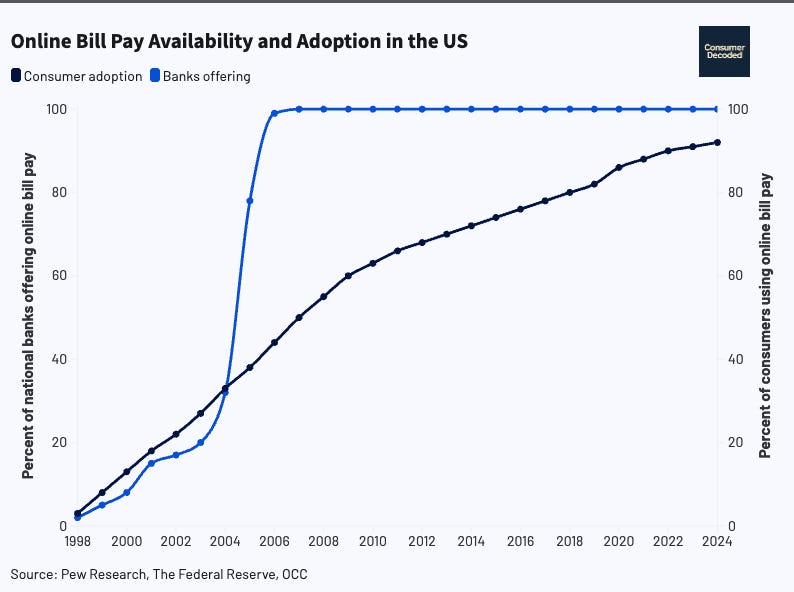

Before the internet, consumers received all of their bills in the mail. They handwrote a check, stamped the envelope, took it to the mailbox, and mailed it in. They could not precisely time payments because there was no predicting how long the mail would take to deliver it. The payer had no confirmation until the recipient cashed the check and they received their monthly banking balance—hence the phrase, “the check is in the mail.”

In the 1990s, ACH technology was introduced to allow electronic fund payments, but it was not until Wells Fargo introduced bill pay function in its app that consumers started to adopt bill payment. Initially, adoption was limited—Wells Fargo introduced the capability in 1995 and by 1998 only 13% of internet users were using online bill pay. The early users followed a familiar pattern—they were younger and wealthier than the average consumer.

By the mid-2000s, nearly every national bank offered the service and consumer adoption grew. Today, online bill pay is nearly universal with almost all banks offering it in the U.S. and the vast majority of consumers using online bill pay. When looking back at initial resistance to adoption, the concerns sound eerily similar—consumers were not sure if they trusted it, they wanted to retain control to avoid overdrafts and they were concerned about having late payments. But as more consumers tried it on low stakes bills and gained comfort with bill payment—and the internet more broadly— usage became nearly universal.

Same Pattern, Different Category

This delegation pattern is not unique to online banking. Other examples include things as simple as navigating to where we need to go. Prior to 1996, you needed to get out a large paper map (or maybe several) to determine your directions to get from point A to point B. Then, MapQuest introduced a new option to put in your starting and ending point online and receive the route, map, and turn-by-turn directions that you could print and take with you. In the mid-2000s, Google Maps came along, followed by mobile phone usage and today, of course, you can easily hop in your car, navigate to where you need to go with live redirection for traffic and alerts on what is ahead. What was once an active decision—how to get somewhere—is now almost entirely delegated to software and most of us would never think to do manually.

Not all delegation sticks

While there are several examples where consumers have gotten increasingly comfortable delegating decisions, there are some that have not taken. One of the most prominent examples is robo-advisors—automated investment platforms that offer lower costs and broader access—yet adoption remains limited. Despite being around since 2008, only 5-15% of American investors have adopted this.

This is one example of a delegation that should have scaled quickly but hasn’t. Amazon’s “Dash” buttons tell a similar story. Designed to simplify repeat purchases, they attracted a loyal niche but never reached mass adoption and were eventually discontinued. In both of these cases, value proposition is clear—but large portions of consumers did not adopt the technology.

The Conditions for Delegation

There are numerous examples of successful automation and delegation in the market and even more that never scale. On the surface, all of these scenarios have a lot in common and it is difficult to distinguish what made online bill pay successful while robo-investing or Dash buttons remained niche. A closer look reveals that there is a pretty predictable pattern in adoption, though. When five key conditions are met, it accelerates, and when three characteristics are involved, it stalls.

It accelerates when:

Decisions are frequent and repetitive

Stakes are low

Preferences are stable

Errors are easy to detect and reverse

Outcomes are consistent (i.e. limited price/quality variance)

And it stalls when:

Identity is involved

Trust is fragile

Or the consumer still wants to choose

Consumers don’t delegate based on how advanced the technology is.

They delegate based on how much they believe they’ll lose by letting go.

One of the important things to note about this framework is that it plays out differently for different consumers. One consumer may have very stable preferences in a category while another does not. Some consumers consider automating their monthly bill pay or snack replenishment order as very low stakes while others want to maintain tight control.

Applying the Pattern to Agentic Commerce

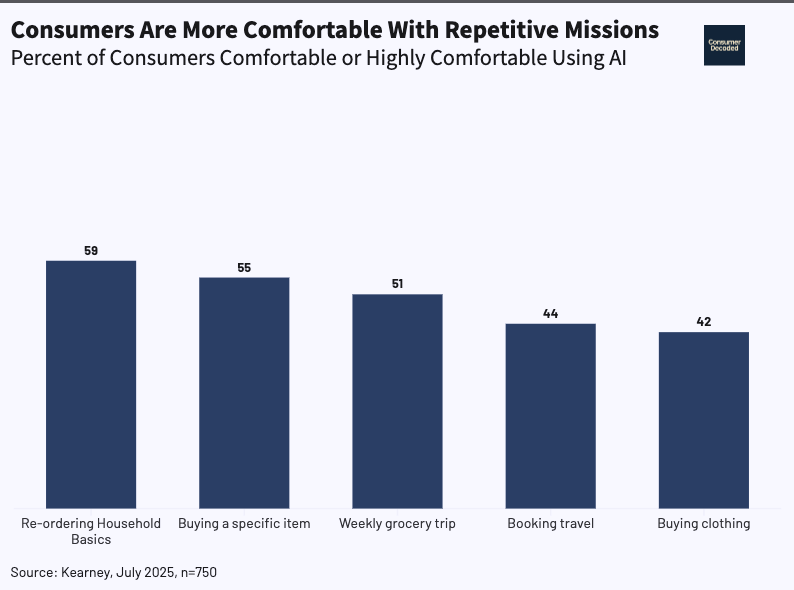

A lot of the debates around agentic commerce right now are about if it will scale and how quickly. The honest answer is: it depends. As we have demonstrated, it really does depend on the decision being made and the consumer making that decision. When asking consumers about their likelihood to adopt agentic commerce for various decisions, their logic follows this line of thinking. Consumers are more likely to automate low-stakes, highly repeatable, stable decisions (e.g. purchasing household goods) and less likely to automate decisions where they believe they add value (e.g. travel).

Much of the current focus is on features like instant checkout. These features are unlikely to have any impact on the categories that convert first.

Technology design could play a big role in accelerating adoption of agentic commerce—the problem is it is not the features that are being discussed broadly today.

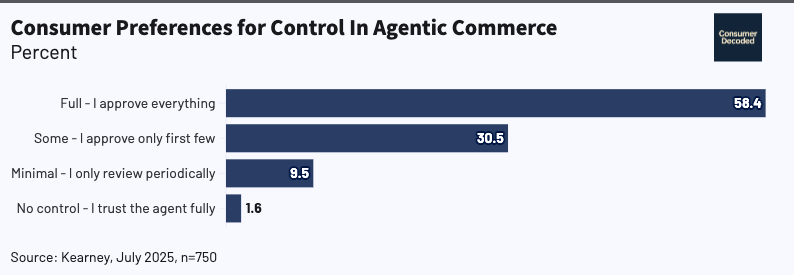

Looking at the pattern of automation adoption and consumer research on the topic, it is clear that technology and infrastructure need to solve for making it easy to detect and reverse errors and ensuring consistent outcomes. These are widely reported issues with the underlying LLM technology today and will require intentional design characteristics to promote adoption. This is one reason that consumers who want to experiment with agentic commerce overwhelmingly want to maintain some control in the transaction initially.

These are solvable problems—but they require intentional design. Engineering the consumer experience so that the consumer can see that they got the best deal, receive confirmation that their order was accurate and met their specifications and creating a clear and easy means to resolve any issues will dramatically accelerate adoption. Meanwhile, instant checkout focuses on removing a friction that barely existed to begin with.

The Bottom Line

Many are wondering if consumers will really delegate their shopping to an agent, but the reality is that they already delegate much of their daily life to automated systems and there is a clear pattern to what they are willing to delegate. Decisions that are repeatable, frequent, stable, low stakes and easy to reverse get delegated at scale. Any decision that does not meet those criteria—or where consumers believe their involvement improves the outcome—will end up being a niche solution. Agentic commerce will scale far faster in some categories—like household goods—and remain niche in others, like travel. Even in categories with high potential adoption, the rate of adoption will depend on how the technology can track and reverse errors as the consumer builds trust in the system.

Interesting Reading:

“The Smartest Minds in AI Just Learned the World’s Most Valuable F-Word,” The Wall Street Journal, March 20, 2026.

“When Using AI Leads to ‘Brain Fry,’ Harvard Business Review, March 5, 2026.

“How Doodles Became The Dog Du Jour”, The New Yorker, March 23, 2026.